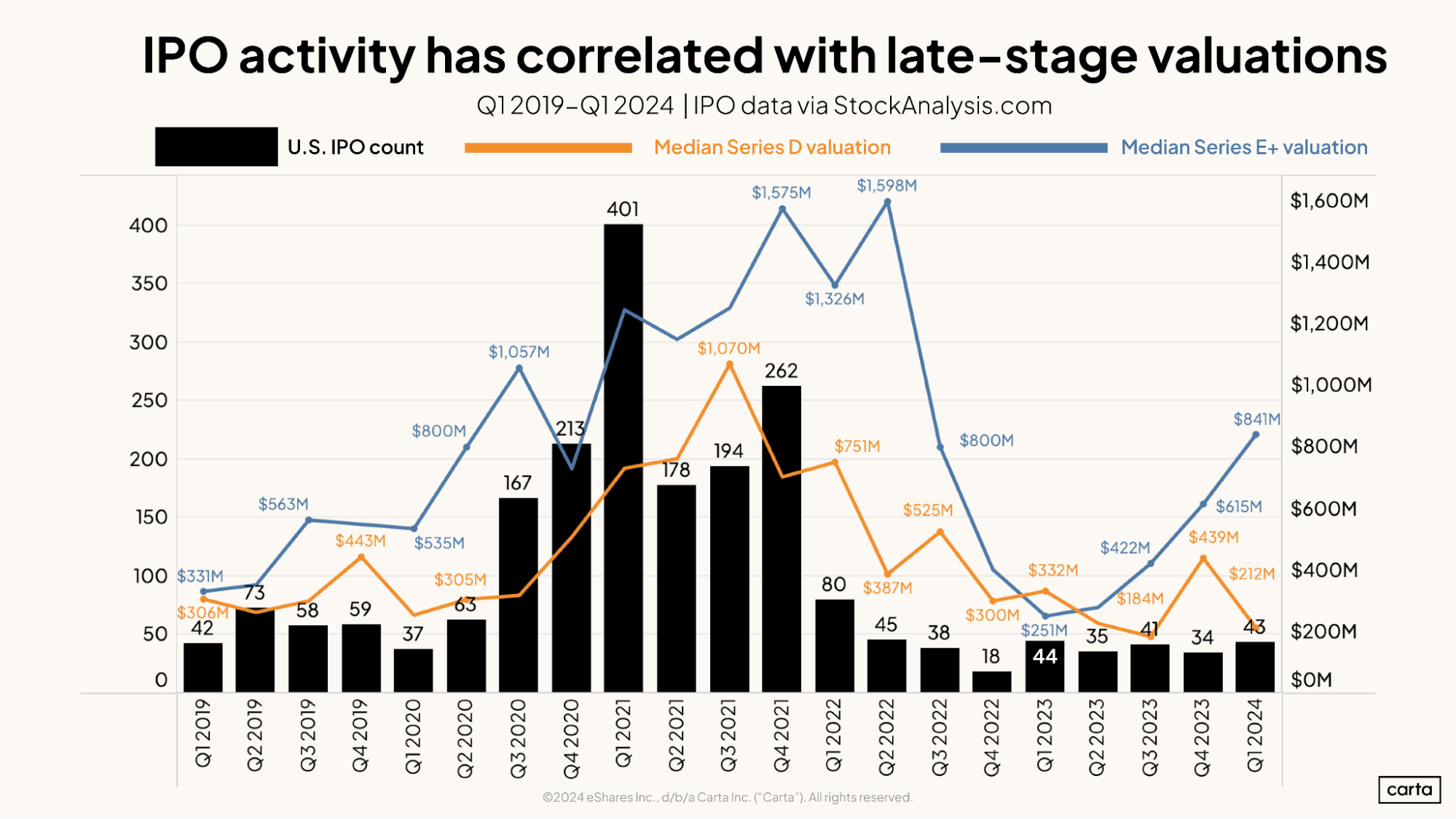

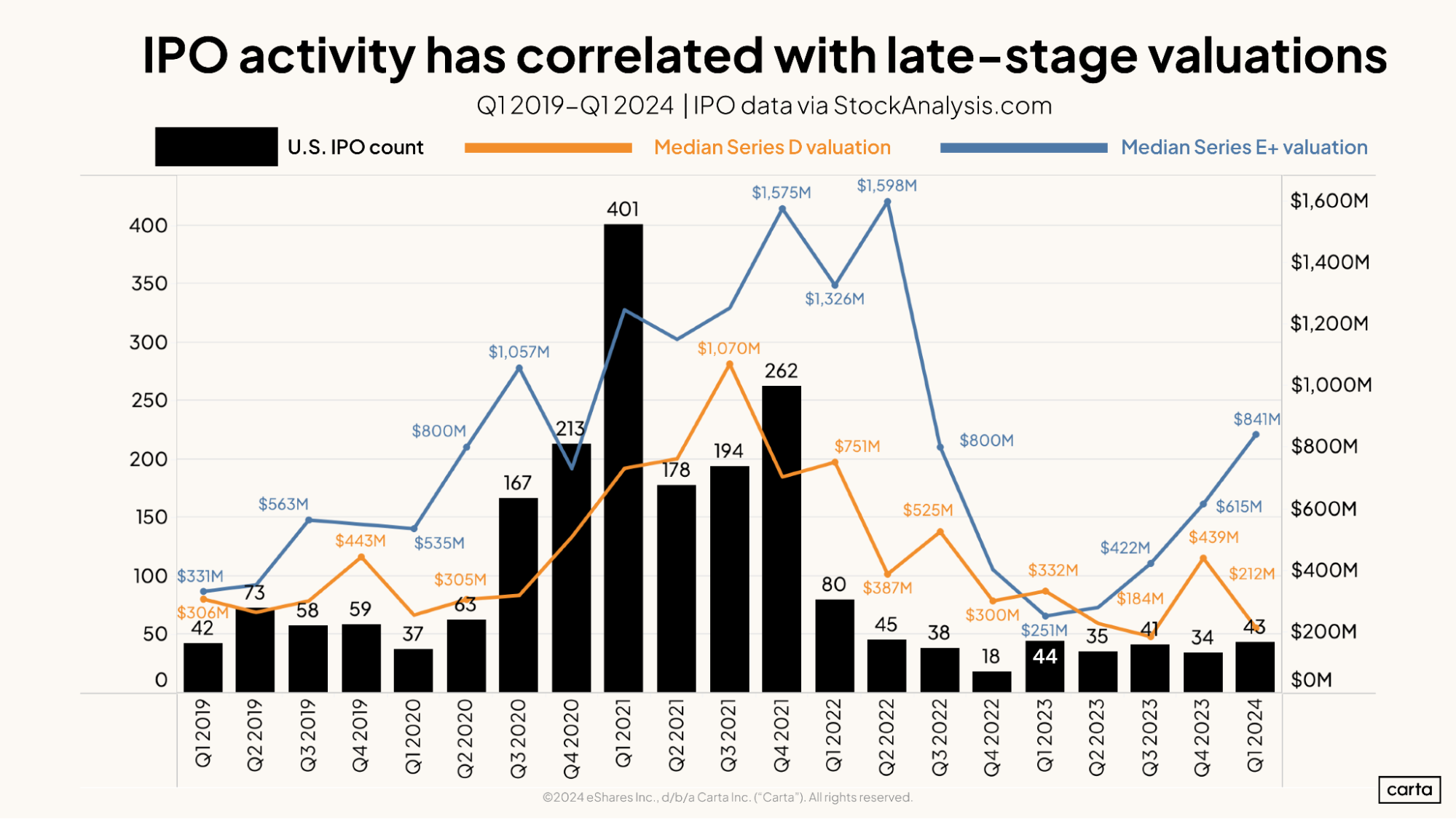

One of the defining features of the pandemic bull market was an explosion in IPO activity. Private companies saw valuations for public companies soar to new highs and raced to join their ranks.

In 2019, there were 232 IPOs in the U.S. By 2021, that number had climbed to 1,035, a 346% increase in the span of two years.

But like so many other aspects of the private capital ecosystem, that burst of deal activity that brightened the market in 2021 soon dimmed. There were just 181 IPOs in the U.S. in 2022, an 83% year-over-year drop, and only 154 listings in 2023. Through June 11, there had been 81 completed IPOs so far in 2024, on pace for a modest 18% increase over the previous year.

This recent dropoff continues a trend: Over the past several years, the number of IPOs in the U.S. has generally tracked closely with the size of late-stage valuations in venture funding rounds. As the number of public offerings got smaller beginning in 2022, so too did median VC valuations at Series D and Series E+.

A market thaw for profitable companies

Isabelle Freidheim is founder and managing partner of Athena Capital, a growth equity investment firm that specializes in backing companies on the brink of an exit. She’s seen a recent shift in the ebbs and flows of IPO activity.

With the recent success of high-profile debuts from companies like Reddit ( up 81% since its debut) and Astera Labs (also up 81%), she thinks it’s clear that IPO investors are ready and willing to buy stock in companies making the transition from private to public—at least, a certain type of company.

“There’s certainly a market opening right now for larger and better-quality companies,” Freidheim says. “Profitability is in high demand now for fast-growing tech companies. Investors have adopted a risk-off approach in the recent environment. Therefore, companies with significant cash needs are out of favor at the moment and unlikely to perform well in the public equity markets."

To Freidheim’s point, Reddit and Astera are perhaps the highest-profile names among a cohort of larger companies that have gotten off to successful post-IPO starts in recent months. Since the start of March, 19 companies (not including SPACs) have raised at least $100 million in IPOs in the U.S. As of this writing, 13 of those 19 companies have seen their stock prices go up in the time since.

“We’ve had a few IPOs now where the quality of the company is high, and the market seems to be receiving them well,” says Adam Nash, a longtime tech executive and angel investor who’s currently the CEO at Daffy, a fintech startup focused on charitable giving.

The need for exits

The broader stock market is also flourishing: The S&P 500 is up more than 13% since the start of January. A combination of rising stock prices and recent valuation successes could encourage some startups to pursue IPOs of their own—which would be a boon to the startup ecosystem.

Profits from IPOs are one of the primary ways that VCs are able to distribute capital back to their LPs. The LPs are then able to reinvest some of that returned capital into new VC funds. And the VCs can then use that capital to invest in promising new companies, beginning the startup lifecycle once again.

“There is very much a need for companies to continue to exit publicly,” Freidheim says. “Access to public exits is the VC industry's raison d'être."

Back in 2021, investor appetite for IPOs extended far beyond the realm of large, profitable, late-stage companies. That sort of extreme environment likely won’t return anytime soon. But Freidheim believes things are headed in the right direction.

“We are bullish on the IPO market in the medium term,” Freidheim says. “We are of the view that the pace of IPOs will resume rapidly in 2025, whether over the second half of 2024 or over a slightly longer time frame.”

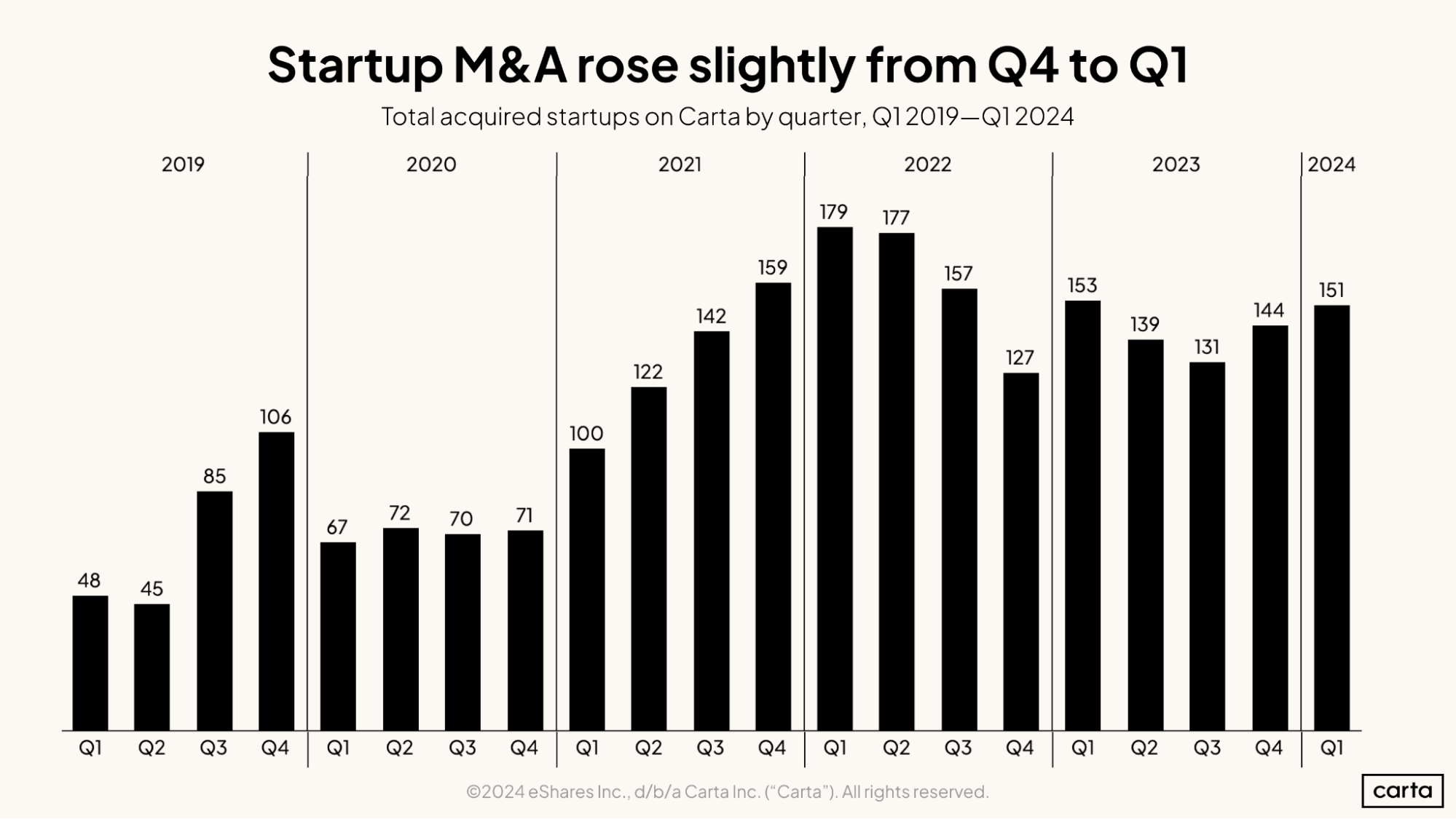

Checking in on M&A

It’s been a mixed start to the year in the market for M&A, the other primary exit pathway for private startups.

Across all M&A transactions types, global transaction value in Q1 was up 38% year-over-year. Total deal count, however, sank 31% compared to the prior year, reaching a nine-year low. Those twin trends show a clear trend in the market toward larger M&A transactions, which would seem to favor larger, more-established private companies at the expense of smaller upstarts.

M&A activity involving startups specifically has stayed mostly steady in the past several quarters. In Q1, 151 startups on Carta were the target of M&A transactions, up about 5% from the previous quarter and down 1% year-over-year.

Freidheim says that she’s seen an increased willingness this year among private equity firms to go shopping among the ranks of venture-backed startups. In some cases those startups are turning to acquisitions as a way to stay afloat in the absence of new VC backing.

“We are observing high activity levels in private equity,” Freidheim says. “Another market dynamic is significant consolidation and roll up activity across tech sectors, including among companies that previously were able to raise capital to compete with each other but who are no longer able to access funding."

Whether it’s IPOs or exits, the story is the same: If investors once again grow less choosy and more eager to invest, it will be a positive development for startups and their backers.

“A lot of the startup ecosystem depends on mergers and acquisitions,” Nash says. “Those big mergers and acquisitions turn into big liquidity events that can create new investors, new founders, and free up capital.”

Get the latest data

For the latest data on venture capital fundraising, startup hiring, compensation benchmarks, and more, sign up the Carta Data Minute: